Buying a New Car – What Are Your 3 Most Common Options for Finance?

More help for you

Pass Your Theory Test The First Time

Preparing for your Theory Test? Sure you can study the manual, but it doesn’t give you a pass guarantee. We do. Pass using our fast and efficient method, or your Premium membership is free.

Discover PremiumInvesting in a shiny new motor can be an expensive undertaking.

If you’re short on cash, you may want to look into ways of spreading the cost in monthly instalments.

Although this can make higher-end models appear affordable, it’s worth doing your homework to ensure that you aren’t paying over the odds in interest -- as this could end up adding thousands of pounds to your repayments.

3 Common Options You’ll Come Across in Car Showrooms

- 1

Hire Purchases

The first type of car finance which is commonplace in dealerships across the UK is a hire purchase. It’s a form of secured loan. Although you will have to put down a deposit to begin with, the rest is paid for monthly.

Check this short video for understanding hire purchase:

There are downsides here: firstly, you don’t have full ownership of the car until everything is paid in full -- and you won’t be able to sell it without the consent of the dealership. You should also make sure that it’s a financial obligation you can sustain in the long run, as the dealer has the right to repossess the vehicle if you miss any repayments. In this regard, it’s not too dissimilar to a mortgage.

- 2

Personal Contract Purchases

Next up, you have the option of making a personal contract purchase. At the end of your contracted repayments, this type of car finance gives you the opportunity to pay off the balance in full and own your vehicle outright -- or, as an alternative, you’ll be able to return it to your dealer in exchange for a newer model. This option generally isn’t recommended if you’re approaching car finance with a view to eventually owning the car.

When it comes to personal contract purchases, bear in mind that companies often set limits on the number of miles you can travel in a certain period. If you exceed this, you’ll likely be charged for every extra mile. What’s more, dealers will demand that the car is kept in a pristine condition and regularly returned for servicing, as they are going to be working on the assumption that you’ll return it for an upgrade later.

- 3

Personal Lease

This is not too dissimilar to the option above, but you won’t have the opportunity to purchase the vehicle at the end of the lease.

The following video provides you with some basic ideas about personal lease.

What Is APR?

This stands for annual percentage rate, and it indicates the cost of your interest over the course of a 12-month period. In some cases, the car finance may come with a 0% interest period, but bear in mind that these deals are often for older or more unpopular models.

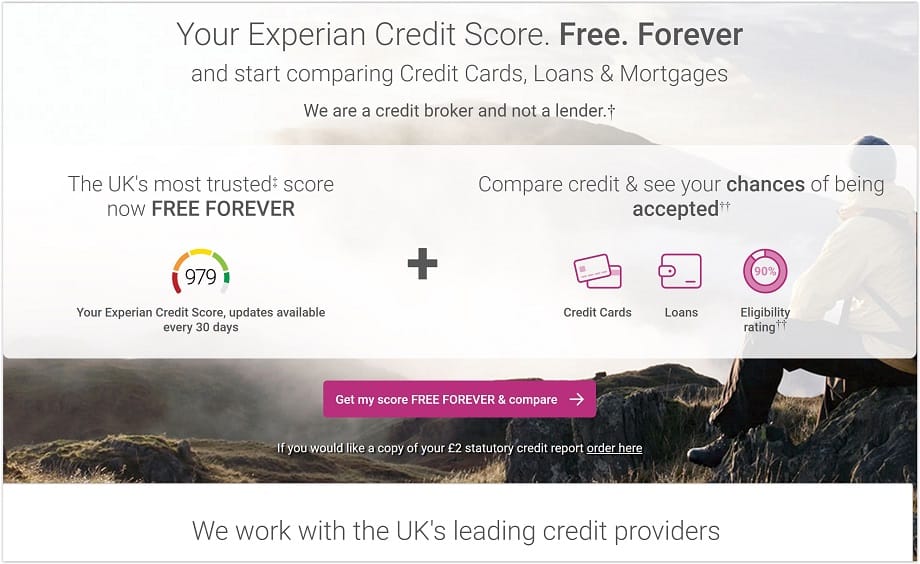

The lowest interest rates are usually offered to people with a good credit rating, and it’s a clever idea to check your score online before you begin looking for deals.

Check your credit rating online. It’s free

In some cases, simple fixes such as getting on the electoral register can give your rating a much-needed boost. Some credit referencing agencies have teamed up with car loan providers, allowing you to check whether you would be eligible for a deal without having to make an application which will be recorded on your credit rating for six years. These records do not indicate whether an application was unsuccessful, but repeated entries can send alarm bells ringing for lenders. Because of this, you’re going to want to be confident of being accepted prior to registering your interest.

There are alternatives beyond getting your car finance from a dealership. For example, your bank may be willing to offer you a loan -- and this enables you to make a purchase without having to pay a hefty deposit upfront. That said, you will lose the perks of being able to trade in your car later, and many lenders penalise those who attempt to pay ahead of schedule. If you intend to make extra payments beyond your monthly requirements, try to look for a company which doesn’t charge extra.

Top Tips for Getting a Good Deal

You should feel free to compare multiple dealers and negotiate interest rates with them, as some companies will have a little leeway that could save you a pretty penny. It’s worth shopping around and it’s ill advised to jump to conclusions.

Check this finacial guide to car finance and choose the option that suits you most:

If you end up going for a loan, do bear in mind that this may affect your ability to obtain credit for other things in the future. Acquiring a mortgage or a credit card could become a little more challenging, and you may be stopped from borrowing as much as you hoped for.

Finally, be aware of pesky little extras which many dealers try to offer because they work on a commission basis.

These include payment protection insurance (which has been subject to a long-running scandal in the UK) and guaranteed asset protection insurance which insulates your car in the event it gets stolen or irreparably damaged in a collision.